Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the all-in-one-seo-pack domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /hermes/bosnacweb04/bosnacweb04ai/b1550/ipg.lantanasolutionsbh98965/economypedia/wp-includes/functions.php on line 6121

Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the google-listings-and-ads domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /hermes/bosnacweb04/bosnacweb04ai/b1550/ipg.lantanasolutionsbh98965/economypedia/wp-includes/functions.php on line 6121

Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the soledad domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /hermes/bosnacweb04/bosnacweb04ai/b1550/ipg.lantanasolutionsbh98965/economypedia/wp-includes/functions.php on line 6121

Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the soledad domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /hermes/bosnacweb04/bosnacweb04ai/b1550/ipg.lantanasolutionsbh98965/economypedia/wp-includes/functions.php on line 6121

Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the soledad domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /hermes/bosnacweb04/bosnacweb04ai/b1550/ipg.lantanasolutionsbh98965/economypedia/wp-includes/functions.php on line 6121

Accounting - Economypedia

Ballon Interest refer to a higher interest that is paid on the longer maturity bonds of a serial bond issue. In other words, a balloon interest refers to paying a higher coupon rate on financial instruments gradually mature at regular intervals until the whole issue matures.

The coupon rate of such bonds is inflated because it is gradually rises over the life of the bond issue, and hence the term balloon.

The Advantage of the balloon interest

Balloon interest allow bondholdersto hold onto debtlonger by reduce that fixed payment amount in exchange for making a larger payment at the end of the loan’s term.

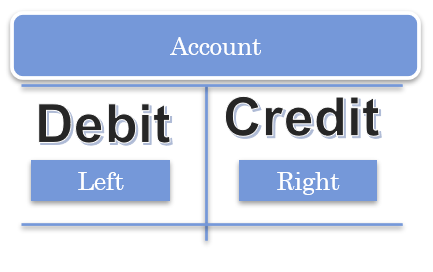

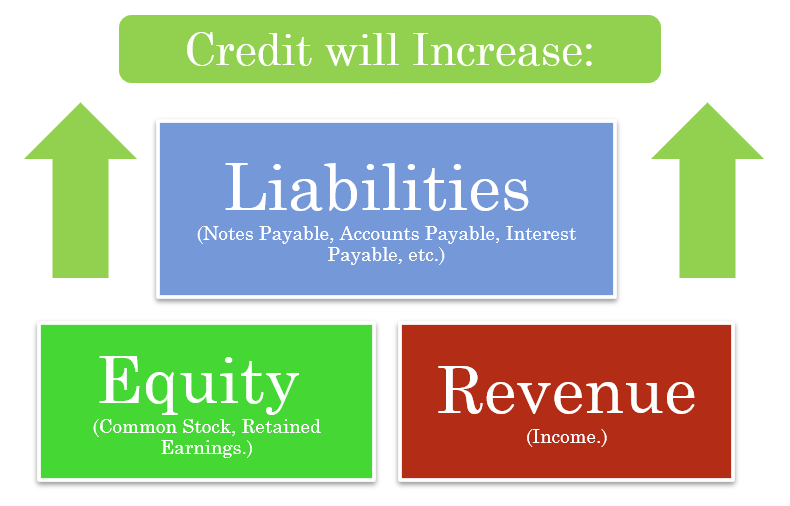

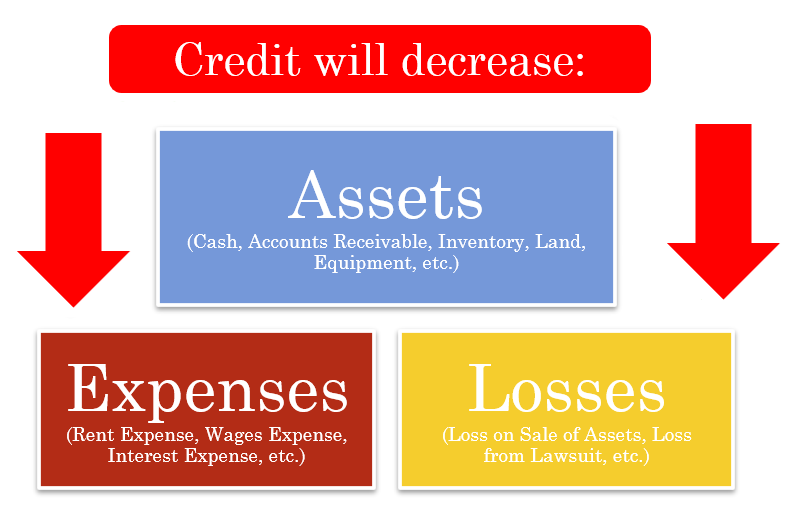

Credit (Cr) is a fundamental accounting entry that used to increases the accounts of Liabilities and Equity, or to decrease Assets and Expenses.

It is positioned to the right side in an accounting entry. On other hand, debit (Dr), positioned to the left side in an accounting entry and work to balance of the accounting entry.

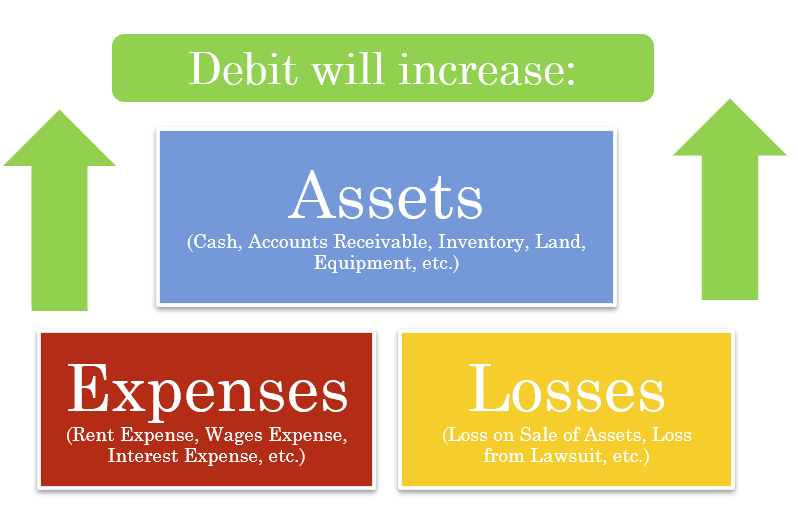

Debit (DR) is a fundamental accounting entry that used to increases the accounts of Assets and Expenses , or to decrease Liability and Equity accounts.

It is positioned to the left side in an accounting entry. On other hand Credit (CR), positioned to the right side in an accounting entry and work to balance of the accounting entry.

Bookkeeping is the process of recording your company’s financial transactions into organized accounts on a daily basis. It can also refer to the different recording techniques businesses can use.

Maintaining and balancing ledgers, accounts, and subsidiaries

Importance of Bookkeeping

Proper bookkeeping gives companies a reliable measure of their performance. It also provides information to make general strategic decisions and a benchmark for its revenue and income goals. In short, once a business is up and running, spending extra time and money on maintaining proper records is critical.

GAAP (Generally Accepted Accounting Principles) are accounting standards, conventions and rules. It is what companies use to measure their financial results. These results include net income as well as how companies record assets and liabilities. In the US, the SEC has the authority to establish GAAP. However, the SEC has historically allowed the private sector to establish the guidance. See The Financial Accounting Standards Board.

In accounting, a financial transaction in accounting is an event that impacts on the monetary value of an asset, a liability, or the owner’s equity of a business and causes it to change. A financial transaction is characterized by the monetary impact it has on the financial statements of the business created by recording it’s details in an accounting register called journals. An event that does not impact on the business financially or monetarily is not recorded in the journals.

What is the purpose of recording a financial transaction in accounting?

Business stakeholders like managers, investors and funders need relevant and timely information to help them make financial decisions about the business resources under their control. In accounting, this information is supplied by financial reports that inform stakeholders of the current financial position and performance of the business. By recording financial transactions that impact on the assets, liabilities and owners equity of a business, stakeholders are able to stay constantly informed of the changes taking place in the financial position and performance of the business.

Financial Accounting Standards Board is a private, non-profit organization that sets both broad and specific principles.

The FASB’s standards are the source of authoritative non-governmental US generally accepted accounting principles (US GAAP)

How was the FASB established? The Financial Accounting Standards Board (FASB) was created by the Securities Exchange Act of 1934 under instruction from Congress to establish accounting principles that would provide transparency to investors regarding business transactions. The FASB was initially created through a joint effort between 3 private organizations: American Institute of Certified Public Accountants (AICPA), American Accounting Association (AAA), and National Association of Accountants (NA).

Why is FASB important?

The stated mission of the Financial Accounting Standards Board is to establish and improve standards of financial accounting and reporting for the guidance and education of the public, including issuers, auditors, and users of financial information.

The accounting standards developed by FASB directly impact how businesses report items such as inventory costs, debt, assets, revenue, stockholder’s equity, and taxation. FASB also allows businesses to choose how they depreciate assets on their financial statements, and they must disclose which method is used and use it consistently for the life of the assets.

FASB requires companies in the same industry to report revenue in the same manner. This helps the public compare each company’s financial statements with the knowledge that the same reporting standards are being used.

Functions of the Financial Accounting Standards Board

The FASB performs a wide range of functions, ranging from creating new principles to educating the general public

Establish reporting standards

The FASB’s most important function is to ensure that accountants and other intermediaries involved in handling financial information create detailed reports, which are then shared with stakeholders. Following a consistent set of standards enables a more efficient market and economy.

Improve accounting standards

The FASB’s mission, advertised strongly on their website, is to continuously update and enable accountants to work with better accounting principles. In the 21st century, the FASB is looking into how technology interacts with the field of accounting so it can utilize some of the benefits it may bring to the world of accounting.

Ensure information is transparent and useful for investors

In capital markets, it is necessary for investors to receive information surrounding a company’s profits and losses. A recent change made by the FASB allows companies to restrict the information that is conveyed to the investors, which may not be as relevant. The rule applies more to biotech and drug companies who conduct trials and testing phases, which may not be as relevant to investors besides the impact of the finished product itself.

Create new accounting principles

The FASB is responsible for creating new principles that improve the system. An example of a newly created accounting principle is the disclosure principle, which gives a company the right to publicize its details and structure of costs incurred in the year.

Enable the general public to be educated on accounting standards

Professionals undergo years of education in order to truly understand the already existing principles and accounting standards. However, FASB makes sure to continually educate and update the knowledge and expertise of its accountants and other professionals to uphold its mission and purpose while also enabling transparency.

The FASB’s main goal is to design new and effective reporting guidelines for all companies that sell goods or services in the United States. Their secondary role includes oversight regarding changes to GAAP (Generally Accepted Accounting Principles) as Congress may request, so they can implement more effective legislation as a result.

The FASB, at the moment, is more focused on making sure companies report their financial facts in a way that is consistent from year to year. The IASB has a broader focus on increasing the harmonization of international accounting standards across countries and establishing GAAP globally.

Accounting: Accounting is the process of recording, summarizing, analyzing, and reporting the financial transactions related to a business

In simple words, accounting can be defined as keeping records of all financial transactions related to an individual or an entity. And then there are pre-defined rules and procedures in the way a transaction should be accounted for. This is what we call debit or credit, income or expenditure, asset or liability. There are then rules on whether it would be an asset or an expenditure and so on.

Accounting refers to the process of identifying, measuring and communicating economic information to permit informed judgments and decisions by users of the information

American Accounting Association (AAA)

Accounting may be defined as the collection, compilation and systematic recording of business transactions in terms of money, the preparation of financial reports, the analysis and interpretation of these reports and the use of these reports for the information and guidance of management

The systematic process used to generate the financial results of a business organization. The result of all the financial transactions of an entity is summarized and recorded in terms of the Balance sheet, Statement of Profit and Loss, and Statement of Cash Flows.

For every business, it is of great importance to determine the cost relating to product manufactured and cost accounting helps the businesses to make costs decision. The results produced can be used to determine what a product should costs.

This accounting is an important branch of accounting that collects, recovers, and restores the financial information as a part of the investigation process. In order to widen its scope, a proper framework defining a set of benchmarks for forensic accounting is in motion.

Accounting Concepts

Separate Business entity concept: While accounting for a business organization, we make a clear distinction in between the business and the owner. All the business transactions are recorded from viewpoint of the business rather than from the viewpoint of the owner. The proprietor is considered to be a creditor of the entity to the extent of capital bought by him.

Double Entry concept: Every financial transaction requires two aspects of accounting to be recorded for example if a firm sells goods worth 5,000 $ this transaction involves two aspects. One is reduction in stock worth 5,000 $ and other receipts of 5,000 $ cash. The record of these two aspects of a single transaction is termed as a double-entry system. According to this rule, the total amount debited will always match total amount credited. The fundamental accounting equation to above rule is:- Assets = Liabilities + Owners Equity

Going concern concept: Accounting assumes that business will continue to operate for a longer period of time in future. In other words, it is assumed that neither there is any intention nor necessity to curtail the business operations of entity. It is on this basis that financial statements of a business entity are prepared and referring to which investors agree upon their decision to invest in the business.

Matching concept: This concept states that the revenues and expenses must be recorded at the same time at which they are incurred. In general, we match the revenues with the expenses incurred during the accounting period. Broadly speaking, income earned during a period can be measured only when it is compared with the related expenses incurred. On the basis of this concept several adjustments are made for prepaid expenses, accrued incomes, etc. while preparing financial of a period.

Financial accounting is a specialized branch of accounting that keeps track of a company’s financial transactions. Using standardized guidelines, the transactions are recorded, summarized, and presented in a financial report or financial statement such as an income statement or a balance sheet.

In simple terms, financial accounting is the practice of accounting for all money going in and out of an organization. It involves recording, classifying, summarizing, and analyzing all financial transactions.

Why Is Financial Accounting Important?

Financial accounting is important for businesses because it helps them keep track of their financial transactions. In turn, they can make sound decisions on how to allocate their resources. In addition, financial accounting helps you communicate your business finances to outside parties such as creditors and investors. The financial statements generated provide all the necessary information to other parties, which will either encourage or discourage them from partnering with your business.

Who uses financial accounting?

External stakeholders use financial accounting to see the current state of business. For example, shareholders will want to see financial reports before deciding to invest in a business. While suppliers need to see a firms’ financial health before extending credit for services. Next, brokers use a company’s financial reports to determine the value of its stocks and shares. And auditors, governments, and regulatory bodies rely on financial reporting to ensure legal and tax compliance.

Financial accounting should not be confused with managerial accounting, which is used internally by managers (hence the name) to help guide decision-making within a business. Whereas financial accounting, as we’ve just established, serves external stakeholders.

Managerial accounting is the practice of using accounting information — from revenues to production inputs and outputs affecting the supply chain — internally, in support of organization-wide efficiency and for tracking the organization’s progress toward attaining its stated goals.

The basic function of managerial accounting is to help the management make decisions. There is no fixed structure or format for it.

What Is the Value Of Managerial Accounting?

While both managerial accountants and financial accountants may occasionally make use of the same data, the scope of managerial accounting is much wider. Managerial accounting supports a broad understanding of cost versus benefit. Managers faced with specific decisions may request information on any number of business operations to chart the best possible course of action.

Types of Managerial Accounting

Product Costing and Valuation Costs can be bifurcated into the variable, fixed, direct, or indirect costs. Cost accounting helps in measuring and identifying these costs as well as assigning overheads to each type of product or service. Product costing, thus, determines the total costs incurred in the production of a good or service. Managerial accounting helps in calculating and allocating overhead charges to assess the expenses or costs related to the production of a good or service. The overhead expenses can be allocated on the basis of the number of goods produced, the number of hours run, the number of machine-hours, the square footage of the facility or any other activity drivers related to production. Managerial accounting also uses direct costs for the purpose of valuing the cost of goods sold and inventory.

Cash Flow Analysis Cash flow analysis helps in determining the cash impact of business decisions. Most companies follow the accrual basis of accounting to record their financial information as it provides a more accurate picture of a company’s true financial position. However, it also makes it difficult to measure the true cash impact of a single financial transaction. By implementing working capital management strategies, one may optimize cash flow and ensure that the company has enough liquid assets to cover short-term obligations. While performing the cash flow analysis, one needs to consider the cash inflow or outflow generated as a result of a specific business decision.

Inventory Turnover Analysis Inventory turnover involves a calculation of how many times the inventory has been sold and replaced in a given period of time. It helps businesses in making better decisions on pricing, manufacturing, marketing, and purchasing inventory. Inventory Turnover analysis also helps in identifying the carrying cost of inventory. The carrying cost of inventory is the amount of expense a company incurs to store unsold items.

Constraint Analysis Reviewing the constraints within a production line or sales process is also a part of Managerial accounting. It involves determining where bottlenecks occur and calculating the impact of these constraints on revenue, profit, and cash flow. This information is useful to implement changes and improve efficiencies in the production or sales process.

Financial Leverage Metrics Financial leverage refers to the use of borrowed funds in order to acquire assets and increase its return on investments. Through balance sheet analysis, the company’s debt and equity mix in order to put leverage to its most optimal use can be studied. Performance measures such as return on equity, debt to equity, and return on invested capital help the managers to identify key information about borrowed capital.