Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the all-in-one-seo-pack domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /hermes/bosnacweb04/bosnacweb04ai/b1550/ipg.lantanasolutionsbh98965/economypedia/wp-includes/functions.php on line 6121

Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the google-listings-and-ads domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /hermes/bosnacweb04/bosnacweb04ai/b1550/ipg.lantanasolutionsbh98965/economypedia/wp-includes/functions.php on line 6121

Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the soledad domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /hermes/bosnacweb04/bosnacweb04ai/b1550/ipg.lantanasolutionsbh98965/economypedia/wp-includes/functions.php on line 6121

Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the soledad domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /hermes/bosnacweb04/bosnacweb04ai/b1550/ipg.lantanasolutionsbh98965/economypedia/wp-includes/functions.php on line 6121

Notice: Function _load_textdomain_just_in_time was called incorrectly. Translation loading for the soledad domain was triggered too early. This is usually an indicator for some code in the plugin or theme running too early. Translations should be loaded at the init action or later. Please see Debugging in WordPress for more information. (This message was added in version 6.7.0.) in /hermes/bosnacweb04/bosnacweb04ai/b1550/ipg.lantanasolutionsbh98965/economypedia/wp-includes/functions.php on line 6121

eco - Economypedia

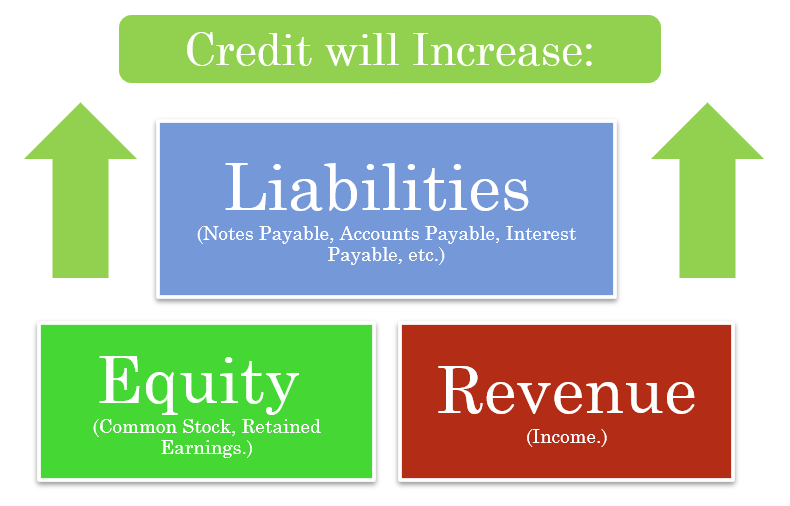

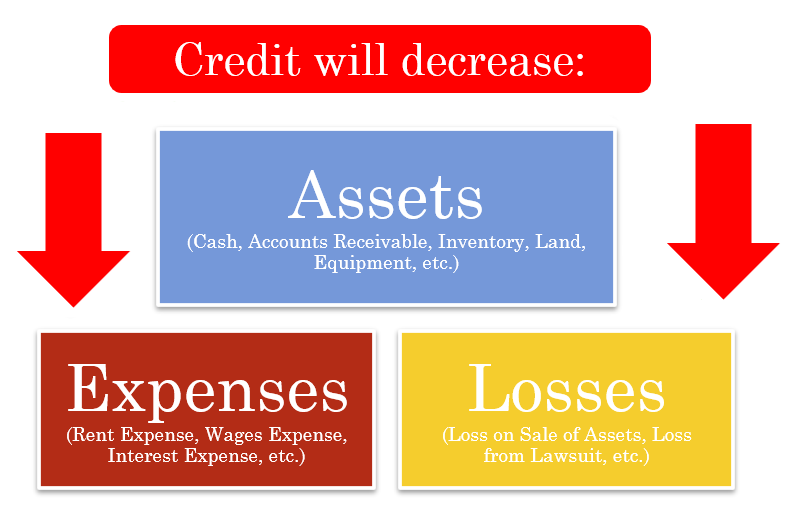

Credit (Cr) is a fundamental accounting entry that used to increases the accounts of Liabilities and Equity, or to decrease Assets and Expenses.

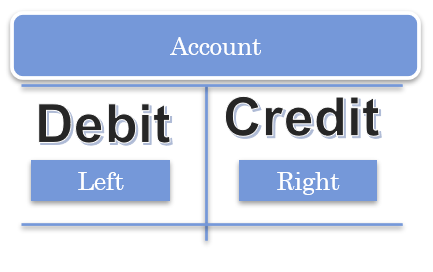

It is positioned to the right side in an accounting entry. On other hand, debit (Dr), positioned to the left side in an accounting entry and work to balance of the accounting entry.

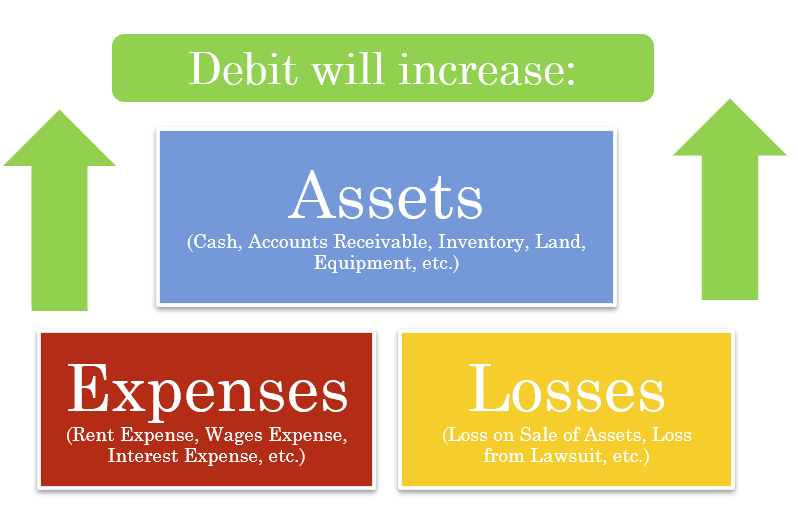

Debit (DR) is a fundamental accounting entry that used to increases the accounts of Assets and Expenses , or to decrease Liability and Equity accounts.

It is positioned to the left side in an accounting entry. On other hand Credit (CR), positioned to the right side in an accounting entry and work to balance of the accounting entry.

Islamic finance is the concept of practicing the financial activities according to Sharia (the islamic law) . though that the original concepts of the islamic finance can be tracked to beginning of the islam back 1400 years ago, the formal islamic finance occurred only in the 20th with launching the islamic banks in Saudi Arabia and united Arab Emirates .Islamic finance grows very fast with range of 15%-25$ per year, increasing the value of the asset which is managed according to the islamic finance rules from $200 Billion in 2003 to oversee over $2 trillion.

According to the Sharia islamic law, which is considered the principles source of the Islamic finance, Some actives are strictly prohibited : 1-Interest Charging. 2-Investing in business activates which are prohibited in Islam. 3-Speculation – gambling (maisir) 4-Uncertainty and risk (gharar)

In additional to two principles of : 1- Transactions must be based on assets and legitimate trade. 2- Risks and benefits should be shared.